Having a great credit score is vital to saving money and creating better financial opportunities for yourself.

Credit scores are a reflection of your financial accountability and responsibility. Thus, businesses, lenders, banks, credit companies, investors, insurance companies, utility companies (cell phone, internet, cable, gas, electricity, and water companies) even employers and landlords may be concerned if you have a less than a good score.

Although most companies do take into account other things such as income, and other factors, you may be denied any one of these services, rent, employment, etc. if you have a bad score. If you have a bad or poor score your interest rates for loans and credit will sky rocket. Having a good or excellent credit score can and will save you thousands, especially if it is on a home mortgage.

There are a few main things everyone should know about credit scores.

- Bad/negative reports on your score are typically there for 7 years (bankruptcies can be on there for 10 years). For example, even though you paid off the collections agency, it will typically remain on the score as a history for 7 years.

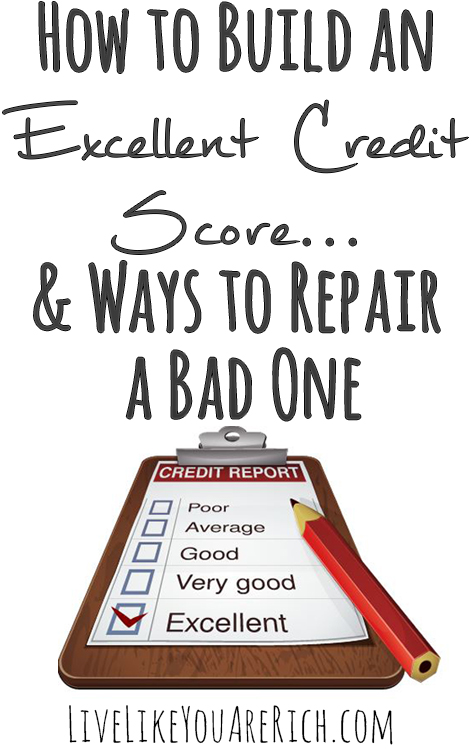

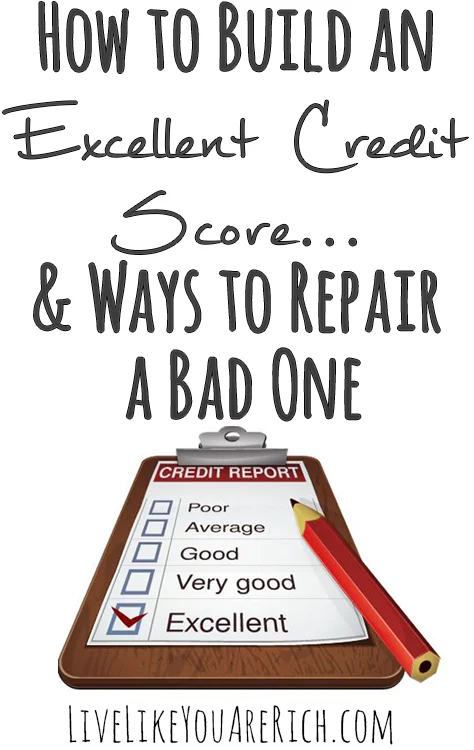

- What is a credit score bracket?

* 750 – 850: A- Excellent

* 700 – 749: B- Very Good

* 660 – 699: C- Average

* 580 – 659: D- Poor

* 300 – 579: F- Worst

- Your payment history and the amount of debt you owe vs. how much credit you have available are the two biggest determiners of your score. Revolving credit debt (such as credit card debt) weighs more heavily against you than personal debt such as a mortgage or car loan.

- Credit Scores include:

* Number and severity of late payments

* Type, number and age of accounts

* Total debt

* Public records

- You can legally receive a free credit report each year. It doesn’t contain the FICO or credit score, you have to pay for that. An awesome service that I use allows you to see your credit reports and scores free is CreditSesame (they will not ask you for a credit card to sign in… it truly is free).

- You can improve your credit score by keeping accounts and credit cards open and paid off for a long time. The longer you have a good standing account the better.

- Closing your credit cards can negatively affect your score. I cut the few up that I have had that does not charge me a fee and just leave them open. The one card that had a yearly fee attached to I did officially close.

- Applying for lots of credit (credit cards, different types of loans, etc.) within a few months of time can drop your score. SEE next bullet point…

- Most people think that checking a credit score multiple times will ding their credit. I thought so too. Recently I read on myFICO.com and found out the following… It isn’t the fact that your credit score is being checked/pulled that will ding your credit, it is why you are applying for the credit that will ding your score. Getting a car loan (multiple car companies pulling your score) shopping for a house (multiple mortgage lenders pulling your score) should not negatively affect your score. They are generally looked at as one pulled report. BUT applying and attaining multiple credit cards (having your score pulled multiple times for different loans) in a short amount of time will slightly lower your score and raise a red flag for future lenders. Source. By checking your credit at a website like Credit Sesame you will not hurt your score either.

How to rebuild a less than great score?

It’s important to realize that by making a few adjustments your score can be positively impacted and be raised within even just a month. That said, negative reports can stay on for 7 years. Certain types of bankruptcies and tax liens or issues can stay on for 10 years. It’s always best to prevent a negative report. If you do have negatives on your report the best thing you can do is start adding as many positives and pay off as much debt as possible. Below you will find practical idea on how to repair a bad score.

- Pay bills on time (set up automatic payments if this is a problem for you).

- Keep accounts open and in good standing

- Pay off any collections

- Lower your debt/credit ratio as best and quickly as you can

- Examine your credit report at least once a year and fix any mistakes that are on it by writing a letter to the credit bureau and reporting company. Mistakes can and are made, these can be disputed.

- Smaller negatives like a late payment on a very low balance can be disputed or requested to be deleted off your report sometimes with success.

- If you are having trouble paying all of your bills using the tips from this website to cut out unnecessary expenses, sell off items, downsize to a less expensive living situation, make more money, budget, take the Financial Fitness Boot Camp Course here, etc. If these things are still not enough, or if you need further advice contact a legitimate credit counseling service.

- Closing accounts can significantly drop your credit score if the account had a high credit threshold and you close it, it will impact your debt/credit ratio significantly and can drop your score a lot. For example, if you have a credit card with a $10,000 limit with a zero balance and you have balances on your other card(s), by closing it you will raise your debt to credit ratio. You may only want to close accounts that are costing you money or that you are not disciplined enough not to use.

- Set up payment reminders

- Don’t use credit cards you don’t know how to pay off. I.E. if you have a credit card you haven’t used for years and you aren’t sure where to go online to pay it off or who to send the payment to, avoid using it.

- If the major concern is your credit score, the best thing you can do is pay off the revolving debt (credit card debt) first.

- Be aware that the higher the credit score you have, the more of an impact a late payment or collection claim will have on it. If you have a 760 score and get a collection claim on your score it can drop it over 100 points! People with lower scores will not be so significantly impacted. Once you have a high score be diligent about keeping on top of payments.

Note: If for some reason a mistake happens (a missed bill) and you do get a letter from a collections agency, usually there is a period of time where you can pay the bill off and they will not report it. Be sure to ask them to not report it if you pay it off immediately.

I paid a company who cashed my check and somehow a mistake happened. I got a call from a legitimate collections agency about the missed payment. I told them I had paid the bill months before. They had me send a copy of the cashed check that I got from my bank. My bank was able to fax it to them that day and they dismissed the claim.

Another experience was simply a bill that I missed. I soon got a letter from a legitimate collections agency and my jaw dropped. I called them up immediately and told them I never even got the original bill. They said if I was able to pay it that day or within the next day or two it wouldn’t go on my record. So I paid it right then. Just know that there is usually a window that collections agencies give until they officially report you to you the credit bureaus. So as SOON as you receive a call or letter make sure to follow up!

Further, be VERY careful. There are many so-called collection agencies that are scams out there. Never give your Social Security information or other personal information to them over the phone until they have verified your name, number, account, who you owe, etc. Check out this post on a collection agency that is a very common US scam collection agency. Monitoring your credit score often through a free service like Credit Sesame will also help you get notified of identity theft.

Want to know how to set your children up to have excellent credit scores? Don’t miss my book: Living a Rich Life as a Stay-at-Home Mom: How to Build a Secure Financial Foundation for You and Your Children

For other ‘rich living tips’ please subscribe, like me on Facebook, and follow me on Pinterest and Instagram.

Derek Dewitt

Monday 5th of November 2018

My wife and I want to buy a home next year, but we are worried that our bad credit will affect our mortgage rate. I like your point about disputing late payments. I will try to find any discrepancies in the reports and see if I can fix any errors like this.

Debbie

Monday 11th of July 2016

Thanks for the great tips! I am now following you on twitter and Pintrest :) I was wondering ... if I have a small (less than $200) debt to a previous landlord that I was unaware on my credit report (my ex-husband said he paid it) and I pay it off and get a 'letter of delete', should that be good enough for me to get a lease in my name again?

Anita Fowler

Thursday 29th of December 2016

I would call the credit bureau and tell them the situation and ask them what you need to do to dispute it or get it off your credit score. Best of luck!

Yvonne Perkins

Friday 24th of June 2016

Thank you so much for your advice

Panhandle Mom

Thursday 31st of December 2015

I divorced after 22 years. The mortgage record that was on my credit history literally disappeared shortly after we sold the farm and paid it off. That adversely affected my score. As a stay at home wife and mother, I had left a well paid profession to care for my second child who had some special needs, I foolishly cut up my one credit card in my own name and closed the account. My then husband "took care" of all finances, or so I thought. After the divorce I found that hospital bills for me and our oldest daughter, who had been diagnosed with MS while a Junior in college, were never paid and were now in collection in our names and on our credit reports. This was a shock, and yes I kicked myself (still do) for not being more hands on and aware of our finances. But, now both my daughter amd I have terrible credit. I was able to buy a foreclosure through the Homepath website for cash, as it was the only way I wouldn't be homeless with my son. But now, I am an unemployed 55 year old woman who cannot return to my beloved licensed medical profession because I was out of it for more than the regulatory board allows, cannot get even a basic job in my relocated state of Florida (NW panhandle in an area where they hire family and friends only), and wonder now if that may not just be due to age (yes they filter by BD and HS grad date on web applications, the 2 interviews I did have were all 20-30 somethings as was the person interviewing) but also due to a poor credit score after reading these articles. Between a rock and a hard place and wondering how to fix this!

Tarah

Friday 30th of October 2015

Several years ago I got divorced. I had always had good credit and bought myself a small house and even a 4 wheeler for me and my son. A month later I lost my job and was on unemployment for 9 months. I tried selling both house and 4 wheeler. Finally told the bank to come get the 4 wheeler. Then I got a job and saved my house from foreclosure. 15 months later I lost my job again and was back on unemployment. This time there was no saving the house. In the middle of all of that I took out a student loan to do online classes and help improve my life. I used some of the money to save my house the first time. I now have a repo, foreclosure, and my student loans have defaulted. Other than that, always paid everything and been a super responsible person. My credit sucks now. I can't even be put on a home loan with my new husband. I don't even know what steps to begin to take to fix it all as I have been in denial, covering my eyes and pretending all that bad stuff didn't exist. Do you have any advice you could give me?

Anita Fowler

Wednesday 4th of November 2015

I'm sorry for theses circumstances that occured. I'd recommend paying off whatever you owe. Revolving credit first (credit cards) then other types of loans. If you still have them and have not filed bankruptcy that is. Next, wait it out and work on establishing good credit reports at the same time. Get a credit card and use it only if you are sure you can pay it off. Carry a balance for a month and then pay it off. Do that a few times a year to show/demonstrate to credit bureaus that you can pay off credit/debt. Put utilities in your name (if possible) and pay those off monthly on time every time. Anything else that you can put in your name to establish good credit while you are working to pay off the debts and waiting for the bad reports to go away will help you repair and improve your credit score. And of course, talking with a credit counselor would help too.